From the 1st January 2025, large companies will need to include a ‘sustainability report’ as part of their annual reporting package. The new sustainability report will include mandatory scope 1, scope 2 and scope 3 greenhouse gas (GHG) emissions reporting.

The Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024 was passed by Commonwealth Parliament and received the royal assent on the 17th September 2024. Meaning, it is now legislation and passed into law.

This Bill will amend the Commonwealth Corporations Act 2001 and require large companies to make mandatory climate-related financial disclosures. Chapter 2M of the Corporations Act 2001 (Cth) outlines the reporting requirements for companies, will be amended to include a ‘sustainability report’ which includes a climate statement.

This article summarises some of the new reporting requirements and the implications for companies.

Where did this come from?

The Paris Agreement is a legally binding international treaty on climate change. It was adopted at the United Nations Climate Change Conference (COP21) in December 2015. Signatory nations, of which Australia is one, submit their national climate change action plans, known as national determined contributions (NDC’s). Australia lodged their NDC with the United Nations Framework Convention on Climate Change (UNFCC) Secretariat in June 2022. This NDC commits Australia to an emissions reduction target of 43% below 2005 levels by 2030. This commitment to reduce GHG emissions is legislated under the Climate Change Act 2022 (Cth). As part of the NDC, Australia committed to new reporting requirements, aligned with international standards for climate-risk for large business.

December 2015 also saw the G20 Finance Ministers ask the Financial Stability Board (FSB) to review and subsequently establish an international taskforce on climate-related financial disclosure (TCFD). The final FSB report (2017) outlined a need for greater transparency and better information to support informed investment decisions and improved understanding of climate related risk.

The foundational concepts from this report have been adopted by the International Sustainability Standards Board (ISSB) and the Australian Accounting Standards Board (ASSB). These concepts also underpin the newly passed Treasury Laws Amendment Bill[1].

[1] https://asic.gov.au/regulatory-resources/sustainability-reporting/historical-development-of-climate-related-financial-disclosures/

The Australia Government Treasury released multiple consultation process on climate related financial disclosures in December 2022, this progressed into several Exposure Draft Bill and then the Treasury Laws Amendments Bill was introduced into Parliament in March 2024.

The intent of this Bill is to allow investors and clients greater transparency to assess a company’s climate-related financial risks and how those companies are managing, planning for and adapting for those climate risks and opportunities.

What does this mean for company reporting?

A company’s annual reporting package normally comprises of the financial report, director’s report, auditor’s report and now it will include, a sustainability report. The sustainability report will consist of a climate statement, notes to the climate statement and the directors’ declaration about the compliance with the climate statement and notes with the relevant sustainability standards.

The climate statement must disclose:

- If there are any material financial risks and opportunities related to climate,

- Any metrics and targets relating to scope 1, scope 2 and scope 3 GHG emissions, and

- Information about governance, strategy, risk management in relation to above.

The climate statements must be prepared in accordance with the current AASB sustainability standards (which are in alignment with international standards). The standards will require a company to disclose information about its climate resilience, assessed under two possible future states. The Australian Securities & Investment Commission (ASIC) state the scenario analysis in the Corporations Act (2001), refer to the following mandated scenarios in the Climate Change Act 2022[1].

[1] https://asic.gov.au/regulatory-resources/sustainability-reporting/for-preparers-of-sustainability-reports/what-should-your-sustainability-report-contain/

Scenario 1: increase in global average temperature of 1.5°C above pre-industrial levels; and

Scenario 2: increase in global average temperature well exceeding 2°C above pre-industrial levels (meaning an increase of 2.5°C or higher).

Scope 1 and scope 2 emissions reporting will be required from the first year of reporting.

“Scope 3 emissions will be required from the second year of reporting.”

ASIC is responsible for administering the sustainability requirements and enforcing compliance. Companies will also need to audit the annual sustainability report. Similar to the obligations of the auditor of the annual financial report.

Who and when do we need to report?

The new reporting obligations will be phased in, starting with the largest companies first (Group 1 entities). The two tables below summarises who and when the reporting starts.

Who |

|

What |

|

When |

|

How | Amendments to the Corporations Act 2001 (Cth). |

It should be noted, the mandatory reporting of scope 1, 2 and 3 GHG emissions is in addition to the reporting established under the National Greenhouse and Energy Reporting Act 2007 (Cth) (NGER).

First annual reporting periods starting on | Large entities meeting at least two of the three criteria | NGER Reporters | Asset Owners | ||

Consolidated revenue | EOFY consolidated gross assets | EOFY employees | |||

Group 1 1 Jan 2025 | $500 million or more | $1 billion or more | 500 or more | Above NGER publication threshold | Excluded |

Group 2 1 July 2026 | $200 million or more | $500 million or more | 250 or more | All other NGER reporters | $5 billion assets under management |

Group 3 1 July 2027 | $50 million or more | $25 million or more | 100 or more | ||

The Corporations Act 2001 (Cth) will use the NGER definition for scope 1 and scope 2 emissions.

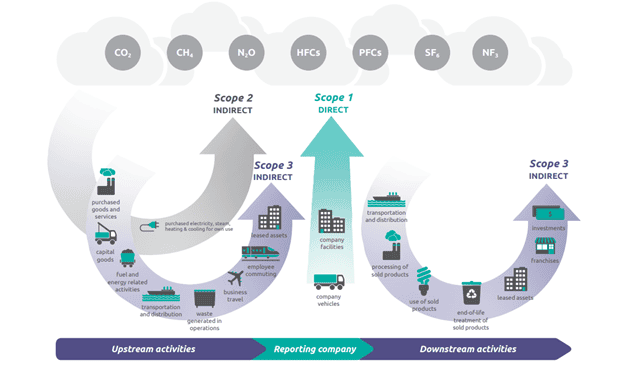

Scope 3 emissions are indirect emissions that occur outside of a company’s boundaries as a result of its actions. They are not reportable under NGER and not very well known. The next part of this article will look a little more closely at scope 3 emissions.

Types of emissions: Scope 1, 2 and 3

GHG emissions reported under NGER include:

- Carbon dioxide

- Methane

- Nitrous oxide

- Sulphur hexafluoride

Scope 1 emissions are released into the atmosphere as a direct result of the activities at your facility.

- Emissions from fuels used in transport,

- Fugitive emissions, such as methane leaks from coal mines,

- Production of electricity by burning coal,

- Emissions from the use of refrigerants in air conditioning units.

Scope 2 emissions are indirect emissions that occur with the purchase of electricity, steam, heat or cooling.

Scope 3 emissions are indirect greenhouse gas emissions (not included in Scope 2) that occur in the value chain of an entity, including both upstream and downstream.

The Treasury Law Amendment Bill Exploratory Memoranda indicates that sustainability report will use the scope 3 emissions categories as outlined in the “Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011)” [1].

[1] ParlInfo – Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024

Scope 3 emissions categories

There are 15 different reporting categories outlined in this definition of scope 3 emissions that companies now must provide metrics and targets against. Not all of the categories will be relevant to your company’s activities.

Scope 3 GHG emissions | |

Upstream – categories 1 to 8 | Downstream – categories 9 to 15 |

1. Purchased goods and services | 9. Downstream transportation and distribution |

2. Capital goods | 10. Processing of sold products |

3. Fuel and energy related activities | 11. Use of sold products |

4. Upstream transportation and distribution | 12. End-of-life treatment of sold products |

5. Waste generated in operations | 13. Downstream leased assets |

6. Business travel | 14. Franchises |

7. Employee commuting | 15. Investments |

8. Upstream leased assets | |

Source: Greenhouse Gas Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard (2011)

What to do next

One way to get started on your scope 3 emissions reporting is to create a value chain map and list all the activities in your company’s value chain. Next ask yourself, do they contribute significantly to your scope 3 emissions? Be sure to document and describe the methodology and assumptions used to calculate the emissions.

If your company is already exempt from lodging a financial report under the Corporations Act 2001 (Cth), you will not be required to prepare a sustainability report.

Small to medium companies that are below the size thresholds of the Group 1, 2 or 3 are not required to make climate statements.

If you are a Group 3 or smaller, you might be sighing with relief at this exemption. However, the companies you work for might be a Group 1, 2 or 3. We except the larger companies will start asking their suppliers for their emissions information, as they will need it to satisfy their reporting obligations.

We recommend getting started on your scope 3 emissions reporting and climate statement journey, as it might just offer your company a competitive advantage when working with the larger entities. The sustainability reporting requirement is new. Starting early with this new challenge will put your company in a better position for new opportunities that may arise.

Let us help you navigate these new requirements

We’re ready to help our clients navigate this evolving landscape. If you require any clarification on anything outlined in this article, please reach out to our Energy Transition Services team. Our skilled team can assist with guiding you through everything from understanding key metrics to developing actionable pathways for compliance.

Send us an enquiry via our ‘Contact Us Form’, or by emailing our ETS Discipline Leader Michelle Gane directly at michelle.gane@engeny.com.au